Capacity markets and energy storage

July 13, 2015.

I've been meaning to get my thoughts together about capacity markets and energy storage ever since the inaugural UK capacity market last year. So here it is, I start by talking about what a capacity market is and aims to do and then think about how it can affect energy storage economics.

The purpose of a capacity market is to ensure that there will be enough powerplants installed and available to generate (sufficient generating margin) for the future operations of an electricity system. The capacity market aims to do this by providing stable and regular payments to market participants who agree to guarantee capacity which can be used to meet peak demand at some point in the future, over and above the payment they receive for the energy that they sell.

Historically the electricity industries in most countries were developed as government owned monopolies. One of the legacies of this is that the wholesale price paid for electrical energy in today's restructured markets doesn't usually include the cost of building the powerplants themselves. Although in today's restructured, re-regulated (liberalised) markets the costs of electricity are nearly always much higher than the marginal production cost (due to a number of factors including utilities' market power), often these costs are not high enough to justify investments in new powerplants. This is known as the 'missing money' problem in electricity markets. Because electricity demand is so variable, and the highest peak demand only covers a short time span and occurs infrequently, electricity systems often have more than sufficient capacity for normal demand levels but insufficient capacity to reliably cover the highest peak demand spikes. If electricity were a more normal commodity, at times of high demand, high electricity prices would cause some consumers to decide they didn't want to buy electricity, which in turn would cause the demand to fall. The 'market price' reached in this situation may then persuade other potential generator operators to enter the market (by building new powerplants). However as the majority of consumers do not see and thus cannot respond to real-time electricity prices, during times of power scarcity, administrative controls often limit the market price to stop it becoming unreasonably high - the demand for electricity is very inelastic. The missing money problem then occurs when the market prices are limited by administrative actions such as price caps. This means that large potential rewards to generators are forgone, and this can in turn result in little investment in new plants which would provide electricity during these times of scarcity.

In an attempt to get around this issue, the capacity market then provides supplementary income to powerplants, in addition to what they earn in the energy market, to cover the costs of ensuring that they are available to generate in future. Capacity (in kW per year) is traded in the capacity market while wholesale electricity (in kWh) is traded in the energy market. The capacity payments are received by the capacity providers in the relevant delivery year and are typically paid for by a charge levied on all electricity suppliers (which in turn is passed on to consumers). There are also penalties for failure to meet a provider's agreed capacity.

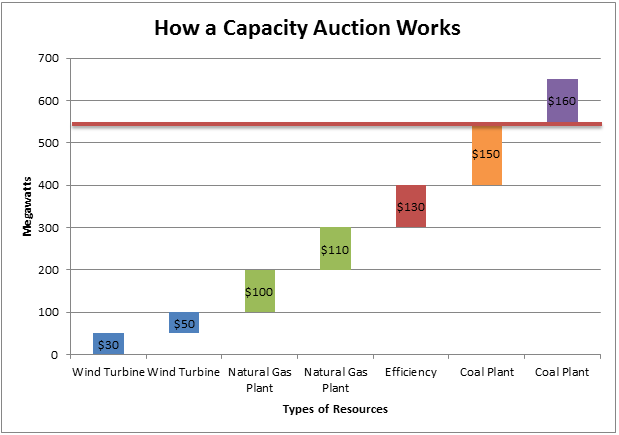

Capacity markets usually include a large primary auction at some specified interval (4 years in the UK) before real time followed by smaller incremental auctions at closer time(s). The price paid for all the accepted bids is the market clearing price - representing the price of the most expensive unit of capacity required. This is known as pay-as-clear. It aims to encourage plants to bid in at their actual marginal cost, rather than speculating what the market price may be. The plant with the lowest marginal cost should then make the largest profit as all the capacity providers receive the same payment. Figure 1 illustrates how the capacity market bids are evaluated.

Illustrating how the "pay-as-clear" capacity market auction works. The red line illustrates the target capacity. All bids below this are accepted and paid the price of the last kW of capacity. Source the energy collective.

One big risk with capacity markets is that they rely on accurately forecasting future demand levels, to determine the optimal level of capacity in future years. If future demand levels are over-predicted, this can result in a large oversupply of capacity and uneconomic plant retirements, burdening consumers with very high costs for reliability. This has happened in Western Australia.

The inaugural UK capacity market was run in 2014 to secure capacity for the winter peak season 2018-19. This is a T-4 auction (four years ahead of delivery) and there will also be a T-1 auction. Capacity providers are free to adjust their positions in private markets from one year ahead of the delivery year and throughout the delivery year, subject to some restrictions. The capacity providers must then be prepared to provide capacity when the system operator issues a capacity market warning. The market rules state that the "System Operator will issue a Capacity Market Warning (CMW) when the anticipated system margin in four hours’ time is less than 500MW. In the event of a System Stress Event starting which was not forecast, a CMW will also be issued. The CMW remains in force until the forecast available margin is greater than the trigger level of 500MW." Once the CMW is issued, providers must deliver their capacity obligation in four hours’ time to avoid CM penalties, should a System Stress Event be active at that time.

Where does energy storage fit into capacity markets?

Capacity markets are often touted as a good potential way for energy storage operators to gain revenue, which when combined with revenues from the energy market, could be sufficient to encourage investment. It has often been observed that the rewards open to energy storage devices in energy-only markets are generally not sufficient (certainly not at present) to justify investment in storage technologies, and the extra income from capacity markets is designed to justify investment in new infrastructure (i.e. generation or storage). Importantly, not only for storage but for all capital-intensive electrical infrastructure, the payments for providing capacity also have the advantage that they represent a reliable source of future income.

However in order to justify investment in new technologies like energy storage, the price reached in the capacity auction must be high enough, and if the price is to reach these high levels then either the level of required capacity must be set high by the system operator (the auctioneer), or some existing resources should not be allowed to enter into the market. Last year, the UK held its inaugural capacity market auction. The auction aimed to be "technology neutral" and nearly all existing generating resources were able to compete, including storage and demand response. The providers were only evaluated at their bid price rather than any other factors, for instance, emissions. The result of this was a price of £19/kW which was too low to for any new energy storage projects.

The real winners of the auction were the incumbent large utilities, whose existing plants got most of the capacity. These plants will be paid the result of the capacity auction on top of what they already earn in the energy market, provided they are still available to operate in the delivery year. This has frustrated many people as it is highly unlikely that many of these plants wouldn't have generated anyway, so the net outcome of last year's UK capacity market seems to have just been a significant increase in consumers' electricity prices for the services they were already getting. What many people see as a problem is that the capacity market did not take into account any environmental factors that would remove, say, coal generation from the auction. DECC had originally stated that nuclear and coal would not be allowed to participate in the capacity auction, but after lobbying from the industry, changed this position.

It seems likely that if capacity markets are to be truly relevant to energy storage, then these markets will have to take into environmental factors like emissions into account. It is fairly obvious that in the short term the costs of meeting our capacity needs are lowest with fossil fuels, however it is the long term cost on society and the environment that these markets should aim to minimise. If we believe in decarbonisation then existing coal plants in particular should not be competing for new capacity payments. In order to encourage storage or other new low-carbon technologies, capacity markets should be further in advance and more ambitious - they should only be open to technologies whose emission levels comply with our decarbonisation targets.

The results of the inaugural UK market imply that the current UK government is much more concerned with security of supply than decarbonisation (although many sceptics say that security of supply has decreased due to our extended dependence on fossil fuels and the result of the auction will be an increase in electricity bills of £1 billion for the same service). Undoubtedly, security of supply is important, but it is, at best, overly-pessimistic to think that security of supply cannot be achieved simultaneously with decarbonisation. An ambitious capacity market would seek to address both of these challenges. Smaller capacity auctions with ambitious environmental targets and higher rewards that look further into the future may be one way to simultaneously achieve both of these aims. In this way these markets could drive up innovation in renewable-storage projects.